Blog Post < Previous | Next >

Guy

Can Walmart hold the line on TV prices?

If increase in tariffs on Chinese TVs stabilize at over 20%, Walmart will have to pass on a brunt of the cost increase to consumers.

The Trump Administration’s trade policy remains highly fluid, shifting from week to week. For that reason, I won’t attempt to forecast the tariff rates that might apply to Chinese electronics.

Other analysts argue that Walmart has enough leverage to pressure its Chinese suppliers into absorbing most of the cost increases associated with new tariffs. In this article, I’ll take a closer look at that claim.

Walmart primarily markets TVs under three brands: Vizio, ONN, and Element Electronics. The first two — Vizio and ONN — comprise the bulk of Walmart’s television sales and are manufactured in China. By contrast, Element Electronics TVs are produced domestically in the U.S.

Vizio and ONN TVs stand out for delivering exceptional value, combining low prices with high consumer satisfaction. Recent listings on Walmart’s website show extremely competitive pricing paired with strong user ratings — often based on thousands of reviews.

BOE Technology (BOE) and Innolux — two publicly traded Chinese original device manufacturers — are among the primary suppliers of TVs and TV components for Walmart’s Vizio and ONN brands. To evaluate their ability to absorb potential tariff costs, we’ll take a closer look at their current profitability.

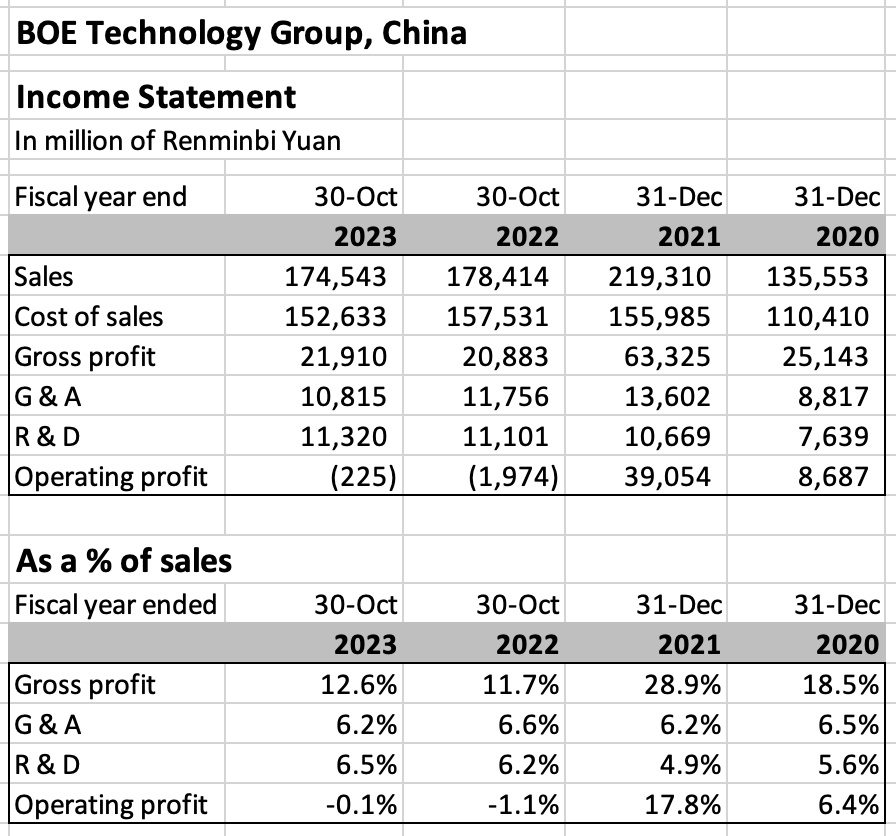

BOE Technology profitability

BOE has not released audited financial statements for fiscal 2024, so I just looked at such statements for the four previous fiscal years.

As illustrated above, BOE’s profitability has declined significantly since 2021. Over the past two fiscal years, the company has operated at a loss. If we assume that BOE’s TV division shares a similar cost structure with the broader company, this suggests that Walmart has already pushed BOE as far as it can on price concessions. Further demands would likely be unsustainable — driving BOE’s margins even deeper into the red.

Innolux profitability

I was able to gather more extensive and more recent financial information for Innolux.

Innolux’s situation mirrors BOE’s — but is arguably even more precarious. The company has posted operating losses for the past three consecutive fiscal years, and in four of the last six. It’s clear that Walmart has already extracted all feasible TV price concessions from Innolux. Given its sustained financial struggles, Innolux’s long-term viability as a supplier is in question. Walmart may soon need to seek an alternative original device manufacturer.

Neither BOE nor Innolux appears capable of absorbing the cost burden of prospective tariffs. That leaves Walmart as the only remaining buffer against higher TV prices. The next step is to examine Walmart’s own profitability to assess how much capacity it has to absorb these added costs.

Walmart’s profitability

Walmart is probably the best managed brick-and-mortar retailer in the US. You can see that on how steady its profit margins have been over the most recent six fiscal years. Within their financial results, you can’t even observe any impact from COVID and its associated brutal recession.

However, despite Walmart’s industry beating financial performance notice how thin its operating profit margins are at around 4%. When you figure interest expenses and taxes, Walmart’s net profit margins are only around 2%. Such profit margins are very low and similar to the grocery industry as a whole. Walmart does have a large % of sales derived from groceries. So, the convergence in margins between Walmart and the grocery industry makes sense.

I would venture that Walmart’s TV business is also associated with very thin profit margins that are not all that different than the ones for the company as a whole.

Given the above, Walmart does not have much of a buffer if any to absorb the impact of prospective tariffs on its TV prices.

Next, let’s run tariff scenarios to figure out how much Walmart would have to raise its TV prices to either maintain its current profitability level or at least break even.

Running Tariffs vs TV Price Increase Scenarios

Below I am running two sets of scenarios.

- The first one entails that Walmart wants to preserve its current profitability level.

- The second one entails that Walmart accepts to just operating at break even for a while. Therefore it has an operating profit margin of 4% it is willing to sacrifice in order to reduce the tariffs impact on its TV prices.

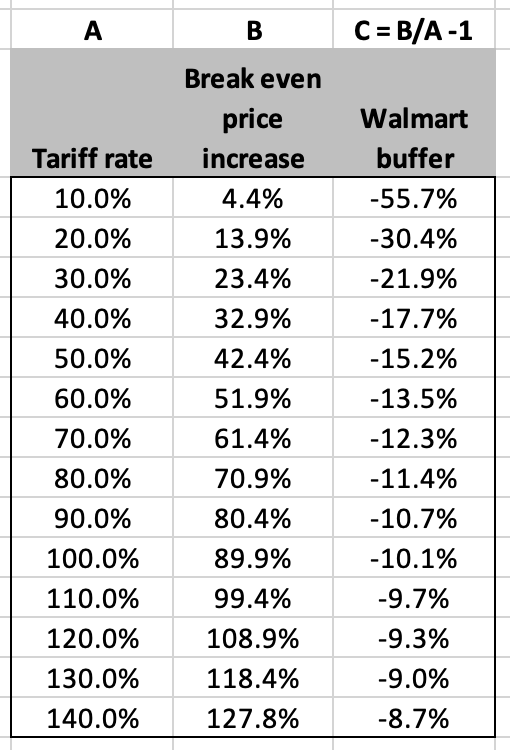

Let’s examine what % of a tariff increase Walmart could absorb by forgoing its typical operating profit margin of 4% and instead operating at break-even on its TV sales. I will call Walmart’s capacity to absorb the tariff rate the “Walmart buffer.”

As shown below, the Walmart buffer is significant when the tariff rate is relatively modest. For example, with a 10% tariff:

(4.4%/10%) −1 = − 55.7%

This means that Walmart could absorb 55.7% of the added cost from a 10% tariff simply by eliminating its TV profit margin and operating at break-even. In such a scenario, Walmart would increase its TV prices by only 4.4% when faced by a tariff of 10% on Chinese TV exports.

However, as tariff rates rise, the benefit of this buffer diminishes quickly — Walmart’s ability to shield consumers from higher prices becomes increasingly limited.

While Walmart is unlikely to operate at break-even on its TV sales over the long term, it could temporarily forgo profits in this category as a strategic move to defend market share and preserve its reputation for low prices. In a highly competitive, price-sensitive segment like consumer electronics, such short-term margin sacrifices can be a calculated decision to maintain customer traffic and brand loyalty.

However, as previously discussed, Walmart would have to absorb the full impact of any tariff-driven cost increases alone. Its key Chinese suppliers — already under financial distress — lack the profitability to share in that burden. This places Walmart in a difficult position: it can either pass higher prices on to consumers and risk losing volume, or absorb the costs and risk compressing its margins or even experience large operating losses on its TV sales if tariffs rise much above 10 percentage points.

From an investor perspective, this dynamic introduces pressure on Walmart’s operating margins and earnings per share, particularly if tariffs persist or escalate. While Walmart’s stock has historically been resilient, prolonged margin compression — even in a single product category — can raise concerns about broader cost pressures and signal vulnerability in other low-margin areas.

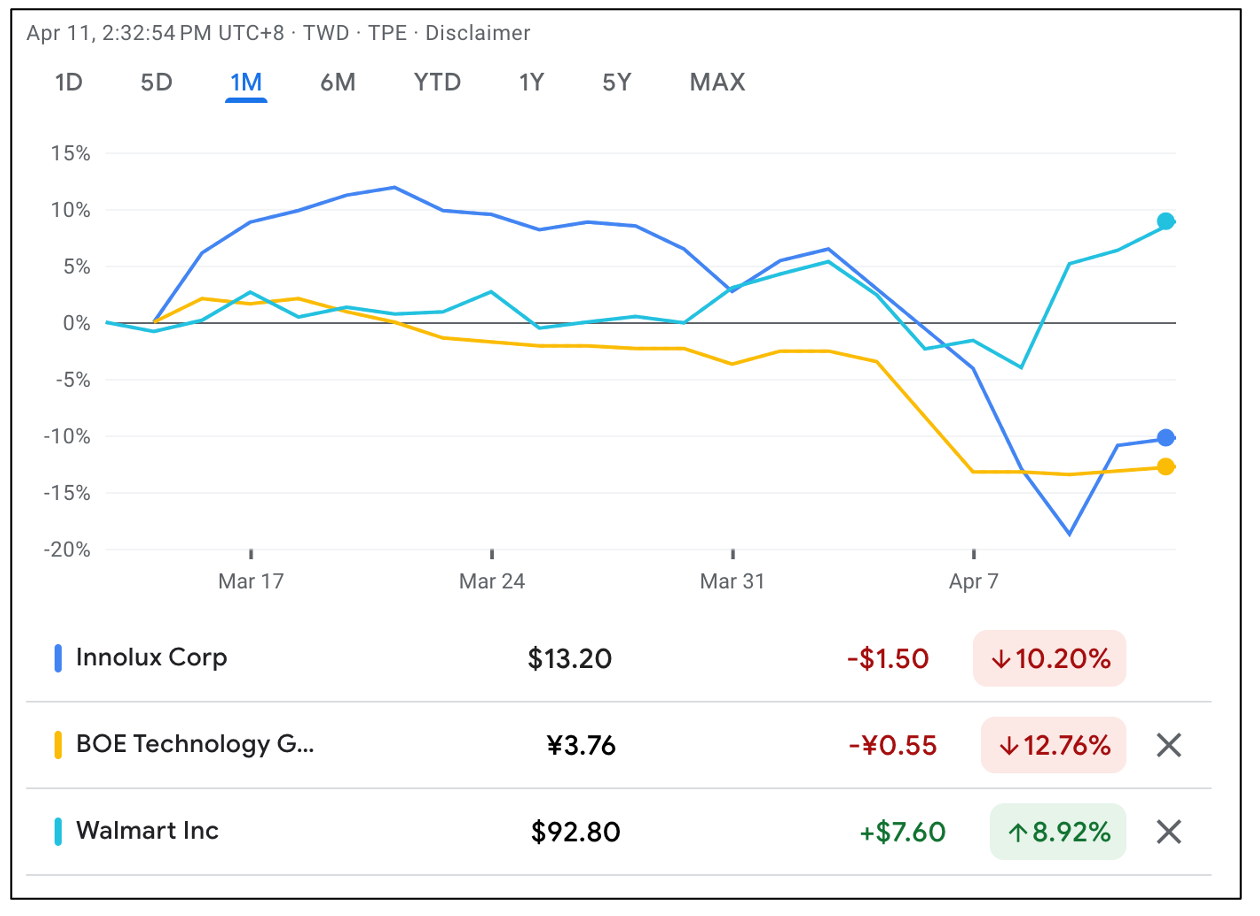

Next, let’s compare the stock performance of Walmart with its Chinese suppliers BOE and Innolux over the recent months.

Stock performance of Walmart, BOE and Innolux

Over the past month the stocks of BOE (orange line) and Innolux (blue) have both dropped by more than — 10%. Meanwhile, Walmart’s stock (green) has actually risen by + 9%.

The stock performance of BOE and Innolux reflects that they are both experiencing substantial financial stress. They have operated at a loss for a couple of years before the Trump Administration even started its chaotic increase in tariffs on Chinese exports.

Walmart’s stock has performed well so far because of its far superior financial strength and steady management. As indicated before, the consistency of its profit margins is most impressive. However, has the market fully priced the uncertainty and ultimate potential outcomes of Chinese tariffs? As reviewed, the latter could really hurt Walmart’s operating margin on its TV sales. And, Trump’s broad based tariffs could impair Walmart’s operating margin company wide.

THE END

Gaetan Lion is an independent researcher with expertise in economics, econometrics, investments, risk management, statistics, and quantitative analysis. His areas of interest include demographics, economics, investments, Climate Change, health care, sports, and politics.